2x Guaranteed Return

with Pramerica Life Rakshak Smart

You Pay ₹50,000 P.A.^

You Get ₹15+ Lac^

Life coverage

Life coverage Policy issuance in 3 days*

Policy issuance in 3 days*

Always Taiyyar

To Protect Your Family

Pramerica Life Rakshak Smart

Get guaranteed* benefits throughout the policy term

Get guaranteed* benefits throughout the policy term

- Choose from two plan options as per your needs

- Avail tax benefits as per prevailing income tax laws

A Non-Linked Non-Participating Individual Savings Life Insurance Plan. UIN: 140N075V03*This plan offers guaranteed benefits provided the policy is in force and all due premiums are paid in full.

15

Years of unwavering

commitment

Protecting 5.2 million lives*

Individual Claims Paid Ratio for FY 31st March 2026 is 99.29%

Individual Claims Paid Ratio for FY 31st March 2026 is 99.29% Pan India Presence

Pan India Presence

You protect a Billion lives,

Leave yours to us

Prahri - Life Insurance for Armed Forces

Coverage of War & War-like Situations

Coverage of War & War-like Situations 100%

Claims Payment Guarantee

100%

Claims Payment Guarantee- Pan

India Presence

Get policy updates on

WhatsApp by texting

'Hello' on +91-9289187070

Call on 1860 500 7070

(Local charges apply)

Call on 1860 500 7070

(Local charges apply) -

Email at contactus@pramericalife.in

Email at contactus@pramericalife.in

Unshakeable life insurance products tailored for your needs

Pramerica Life

Super Investment Plan

- Benefit from Zero premium allocation charge in all years

- Return of Mortality & Waiver of Premium Charges on survival till the end of the Policy Term

Pramerica Life

Cancer + Heart Shield

- Covers different stages of Cancer and Heart conditions

- Monthly Income payable as recuperation benefit to meet your needs.

- No need to pay any premium from the date of first claim for next 3 Policy years

Pramerica Life

Rakshak Smart

- Flexibility to choose from two plan options

- Flexible Premium Payment Modes

- Comprehensive death benefit in Enhanced Life Option

Pramerica Life

Rocksolid Term Insurance

- Guaranteed RockSolid protection throughout the policy term

- Option to pay premiums once, for a limited period or throughout the policy term

- Option to enhance your protection cover against death, disease and disability through riders

Why choose Pramerica Life insurance?

99.29% claim paid ratio

Individual Death Claims Paid Ratio as per audited financials FY’26

125 Branches PAN India

As reported on 31st March 2026

Safeguarding 70 Lakh+ rising Indians

(Group+Individual) in-force lives as on March’26

Need assistance?

We are happy to help you. Talk to our expert and choose the right plan as per your needs.

Simplified Settlement of Death Claims due to recent Floods in affected areas of Assam

We at Pramerica Life Insurance express our heartfelt condolence to all the families affected by the devastation caused due to floods in the state of Assam.

Guidelines on Insurance claims relating to natural disaster affecting four districts of Assam, viz. Sivasagar, Charaideo, Jorhat and Golaghat

Congratulatory Quote on Accounts Aggregator Foundation Day

On Accounts Aggregator (AA) Foundation Day, we congratulate the AA Ecosystem for making financial data sharing safe, simple, and consent-driven. We see the AA Framework promoting the use of data, analytics and technology for designing insurance products that are more affordable, accessible, and tailored to people’s needs. In 2025, the use of AA increased in the insurance sector, particularly for underwriting term insurance policies, and we encourage more insurance companies to experiment and innovate using the powerful DPI rails. This DPI is poised to play a key role in ensuring that every Indian family has adequate protection, and we achieve the country's objective of “Insurance for All by 2047”.

Ajay Seth

Chairperson, IRDAI

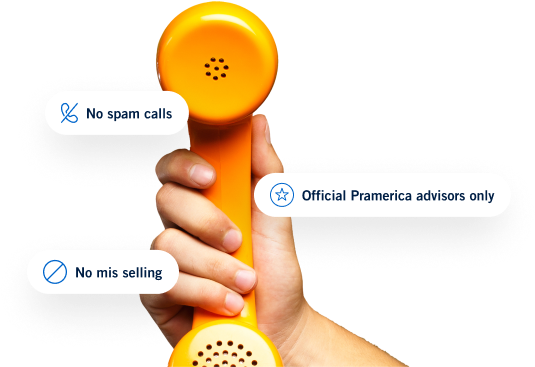

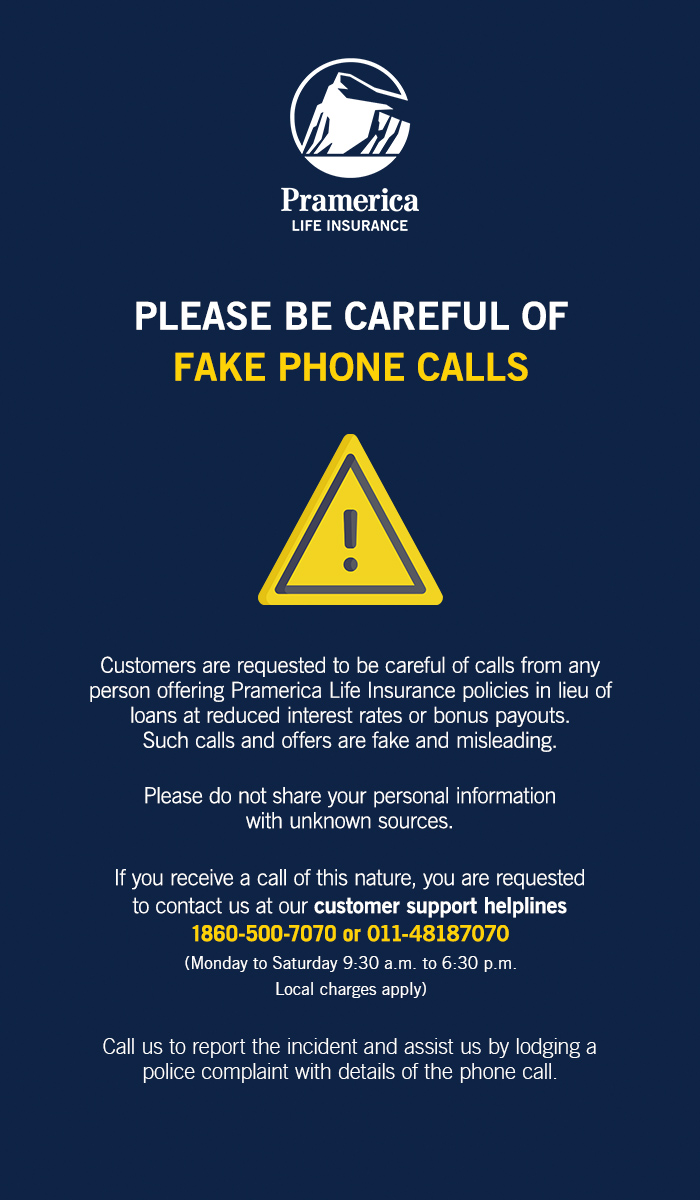

Beware!

Do Not Entertain Fake Phone Calls

Be cautious of calls offering Pramerica Life insurance as loan substitutes with lower interest or bonus payouts

Create Your E-Insurance Account Today

-

Manage policies with ease

-

Instant updates

-

24/7 help & support

Get Policy Updates on WhatsApp

+91 9289187070

+91 9289187070- Manage policies with ease

- Instant updates

- 24/7 help & support

We Value your Feedback

Got a minute ?

We would love to hear about your experience with IRDAI's call center

IRDAI's Call Centre Feedback Survey

A knowledgeable you is an informed you

.jpg) ULIP

ULIP

What are the different kinds of ULIP charges?

People have started taking investment planning very seriously from a young age. However, with so many options out there, selecting the right option as per individual needs remains a risk. Read More

- 12525K View

- 2 min read

.jpg) ULIP

ULIP

5 Essential Features & Benefits Your ULIP Plan Must Have

Are you considering insurance but don’t want your money to sit idle after paying heavy instalments? We get you, especially when the cost of living is increasing every few days while salaries are shrinking. This creates the need for a financial tool that offers good value for money. Read More

- 8483K View

- 2 min read

ULIP

ULIP

Explore Effective Tax Planning with ULIP

You work hard to earn and grow your income. As the financial year comes to a close, tax deadlines can feel overwhelming. Many people rush to find last-minute tax-saving options during January to March. In that hurry, you might choose products that only lower your tax bill. But do they also help you build long-term wealth or protect your family? Read More

- 171K View

ULIP

ULIP

Are ULIPs Good for Kids, Seniors and Women? 5 Surprising Facts You Didn’t Know

When it comes to planning, it is often suggested that one should ideally invest in a plan that offers life cover and also market linked growth in one plan. So the fundamental question arises - What are the benefits of ULIPs that make it more attractive than other more accessible investment options like traditional savings or other market-linked funds? Read More

- 153K View

ULIP

ULIP

Best Plan to Invest for Your Child’s Future: How ULIP is different from Mutual Fund?

Many aspiring students wish to study at a foreign university, knowing it can open doors to high-paying jobs and global career opportunities. With easy access to the internet and vast information resources, your child may have an expectation from you, with respect to providing funds for pursuing higher studies abroad. Read More

- 135K View

ULIP

ULIP

Guaranteed 10% additions - But Is There a Catch? What You Need to Know About This ULIP

Investors are wary about where their money is being parked or what the hidden terms are in any investment scheme. Certain long-term investment instruments like ULIPs promise life coverage based on how the plan is structured. ULIPs, by design, make sure that a part of your premium gets allocated to life coverage and the remaining portion goes to market-linked investment funds. It is an insurance-investment product. Read More

- 161K View

ULIP

ULIP

Planning Your Retirement? Why a ULIP Could Be Your Secret Weapon

A recent report1 has suggested that many Indians have not been saving enough to build a retirement fund. Additionally, a survey by Grant Thornton Bharat revealed that 76% of the respondents2 have not subscribed to any annuity plans for retirement and many believe that existing options are inadequate. Read More

- 126K View

Saving

Saving

All You Need to Know About Basics of Investing & Saving

Financial freedom is not just a dream, but an easily achievable reality. Constant investment and savings habits can help you materialise this dream in no time. Read More

- 6336K View

Saving

Saving

What is a Rider on a Life Insurance Policy

The phrase "one size fits all" does not apply to a life insurance policy. People have different lifestyles and financial requirements, emphasising the need for a customisable plan. Read More

- 13724K View

Saving

Saving

Calculator: How Much Life Insurance Do You Need?

For most people, the biggest question while buying life insurance is how much coverage is enough. If the cover amount is too little, it leaves the family vulnerable, unable to manage daily expenses or long-term goals. Too much coverage, on the other hand, means paying higher premiums that stretch your budget unnecessarily. Both situations can create financial stress instead of solving it. So, it is necessary to create a balance between the two. This is where Pramerica Life Insurance assists you and provides a personalised plan that suits your goals. Read More

- 289K View

Saving

Saving

How Do Guaranteed Payouts Secure Your Family’s Needs?

There are many families in India living with constant financial uncertainty. Sometimes, the rent and basic necessities eat up all their salaries and there are no savings for other investments. Many families can barely build an emergency fund in case of any serious healthcare emergency Read More

- 104K View

Saving

Saving

How to Start Investing as a Beginner?

As a beginner who’s looking into investing, the entire journey of investing might seem daunting. You may have heard of that market swings can lead to losses or that uncertainties can erode any initial investments. So, here we bring investing guide for beginners that can help you start your journey to building corpus. Read More

- 110K View

Frequently asked questions

What is Life Insurance?

Life insurance is a contract that pledges payment of an amount to the person assured (or his nominee) on the happening of the event insured against.

- The contract is valid for payment of the insured amount during:

- The date of maturity or

- Specified dates at periodic intervals or

- Unfortunate death if it occurs earlier

Among other things, the contract also provides for the payment of premiums periodically to the company by the policyholder. Life insurance is universally acknowledged as an institution which eliminates risk, substituting certainty for uncertainty and comes to the timely aid of the family in the unfortunate event of the breadwinner's death. Life insurance is concerned with two hazards that stand across the life path of every person:

- That of dying prematurely leaves a dependent family to fend for it

- That of living till old age without visible means of support

Which policy should I choose?

Your need for protection and planned savings at a point in time is the determining factor when you consider the insurance options. Our salesperson will assist you in making the right choice. However, while your advisor will recommend a life insurance policy that they think will meet your needs, you need to carefully examine the recommendations to ensure that your financial goals and protection requirements are indeed met. In India, the IRDAI has made it mandatory for insurance companies to provide each of the customers with an "illustration" that provides details of the premium outflows and the expected inflows for insurance products tailored to meet your specific requirements. Ask your advisor to explain the illustration to you and clear any doubts you have.

Are my existing policies enough for me? (I already have life insurance policies; what should I do?)

Your need for protection is not fixed as life progresses; new developments happen, and these developments impact the extent to which you need protection. Hence, the requirement for protection should be reviewed periodically, and if there is a shortfall, it should be covered as soon as possible by buying additional insurance cover. For illustration, some of the events in your life that are likely to have an impact on the levels of protection that you need are:

- You or your children are getting married.

- You have become or are becoming a parent

- Your parents or spouse have retired/are retiring and are / will be financially dependent on you.

- The health of your dependents or your health has taken a downturn.

- You have acquired large capital assets like a new home or a car.

- Your children are about to enter school or college.

- You or your spouse has a large salary raise, or the family income levels have significantly increased.

You should consult your agent/ financial advisor if any events like those mentioned above have happened to evaluate if your need for protection has changed.

How much life insurance do I need?

The need for life insurance is based on various factors, including your current lifestyle, expected outflows in future, your present age and your family size. The first step should be to estimate how much financial support your dependents would need to continue to enjoy the same lifestyle as they enjoy today if you are not around to provide that support. In estimating this support, you should consider all regular monthly expenses, including food, rentals, conveyance, school fees, medical expenses, any debts to be repaid, etc., and also estimated ones like children's education and marriage and your expected needs after retirement. Always provide for unforeseen contingencies that your dependents might need during the period of adjustment. Based on this analysis and the expected returns on the investments in future, you can work out a sum of money that would help your dependents achieve financial independence even if you are not around to support them. While every individual's situation would be different and should be evaluated separately, one rule of thumb is to buy a cover for an amount equal to 6-10 times your annual income. The need for insurance is not static and will change as your life stage changes, so you must re-work the requirement periodically and review the coverage available occasionally. It is advisable to speak to a trained financial consultant/insurance advisor to determine the extent of coverage that you require.

Why is it better to buy insurance at an early age?

There are many advantages of buying an insurance policy as early as possible:

- The consideration for an insurance policy or the premium is significantly lower at younger ages (the reason for that is as you grow older, the mortality risk is greater, and hence, insurance companies would charge a higher premium to cover that risk). By buying a policy at an early age, you would be able to protect your dependents against an unforeseen event like death at a much lower overall cost.

- As you grow older, you will likely suffer from health problems, and obtaining insurance could become difficult at that stage, even if you want to.

- If you are buying insurance with a view to create a large sum of money at a pre-determined age to meet certain planned expenses like your childrens education or for your post-retirement expenses, then saving early on in your life is highly beneficial.

If you start saving late, you must keep much more or for longer durations to get the same amount of money.

Who can buy a policy?

Any person who has attained majority and is eligible to enter into a valid contract can insure themselves and those in whom they have insurable interest.

Policies can also be taken, subject to certain conditions, on the life of one's spouse or children. While underwriting proposals, the insurance company considers certain factors, such as the policyholder's state of health, the proposer's income, and other relevant factors.

Why do I need life insurance?

Life is uncertain, and it is impossible to predict the different events that can occur. However, there is always a need to earn income to support yourself and your dependents in case of any eventuality. Life insurance provides financial security in the wake of unfortunate events like death or the inability to earn due to physical disabilities. Besides providing financial protection in the case of one's untimely death, it can be used to accumulate a kitty for your old age, build assets systematically, fund your child's education, and save on taxes.

What are IRDAI guidelines pertaining to claim processing?

As per IRDAI (Insurance Regulatory Development Authority of India), the insurance company is required to settle a claim within 15 days of receipt of all requirements. However, if the claim warrants further verification, the Company should complete its procedures within 45 days from receipt of written intimation of the claim. If the Company settles the claim beyond 45 days period, interest is payable by the Company on the claim amount. The interest is payable only where the claimant has submitted all the requirements. Further, rate and period of interest are decided as per IRDAI guidelines.

How does a Claimant communicate his / her dissatisfaction with regards to his claim decision?

For any clarification, complaint or dissatisfaction claimant / nominee can contact Grievance Redressal Procedure Customer Service Help Line: 1860 500 7070 / 011 4818 7070 (Local charges Apply) (9 am to 7 pm from Monday to Saturday)

Email: contactus@pramericalife.in

Website: https://pramericalife.in/contact-us

Communication

Address:

Customer Service,

Pramerica Life Insurance Limited,

7th & 8th Floor, Tower 2,

Capital Business Park, Sector 48, Gurugram,

Haryana – 122018

How will the claimant receive the claim payout?

As per IRDAI circular no. IRDA/FA/CIR/GLD/056/02/2014 dated February 13, 2014, all payouts made to customers need to be in the electronic form. Hence, we will disburse claim payments through NEFT.

How will I be informed of my claim decision?

You will receive a letter from us on your communication address as soon as we decide on the claim.

Will I need to submit additional documents?

In addition to the listed documents, we may call for additional documents if a need arises.

Why is it essential to submit all the records / documents as required by the company?

Claims are examined and settled by the company basis details present in the documents submitted by you. Hence, it is advisable to provide complete details and all documentation to us for faster and smoother claims processing.

Where should I submit my claim documents?

You can submit the claim-related documents to us at any of our Pramerica Life branches. You may find list of branches in the Locate Us section of our website.

Where can I get the claim form?

- Visit the nearest Pramerica Life branch

- Talk to your Pramerica Life Insurance representative

The nominee is not alive. What should I do?

Please provide a copy of the legal heir certificate for us to process the claim.

I have lost my policy bond. What should I do?

Please provide an indemnity bond on a Rs. 100 non-judicial stamp paper, signed by the claimant. The indemnity bond is available with our branches.

What is rupee cost averaging?

Everyone who invests in the market wishes to get the maximum out of the market by buying at a low price, selling at a high price and timing the market to perfection. However, this is only in theory. In the real world, often, the reverse happens, and investors get caught at the wrong end. To avoid the risk of mistiming the market, rupee cost averaging can be very useful. In this, you invest a fixed sum periodically, say, monthly, over a long term, say a year or two. This lets you enter the market at various price points, irrespective of the market being high or low. In this way, you can average your investment cost and reduce the risk of the ups and downs of the market.

What are the charges, fees and deductions in a ULIP?

Broadly, the different types of fees are given below:

| Premium Allocation Charge | This is a percentage of the premium appropriated towards charges before allocating the units under the policy. This charge usually includes initial and renewal expenses apart from commission expenses. |

| Mortality Charges | These are charges to cover the cost of insurance coverage under the plan. Mortality charges depend on factors such as age, amount of coverage, state of health, etc. |

| Fund Management Charges | Charges These are fees levied for managing the fund (s) and are deducted before arriving at the Net Asset Value (NAV). |

| Policy Administration Charges | These are the fees for the plan's administration and are levied by unit cancellation. This could be flat throughout the policy term or vary at a pre-determined rate. |

| Surrender Charges | A surrender charge may be deducted for premature, partial or complete encashment of units wherever applicable, as mentioned in the policy conditions. |

| Fund Switching Charge | Generally, a limited number of fund switches may be allowed each year without charge, with subsequent switches subject to a charge. |

Are investment returns guaranteed in a ULIP?

Investment returns from ULIP are not guaranteed. In unit-linked products/policies, the investment risk in the investment portfolio is borne by the policyholder. The policyholder may achieve gains or losses on their investments depending upon the performance of the unit-linked fund (s) chosen. It should also be noted that the past returns of a fund are not necessarily indicative of the future performance of the fund.

What is partial withdrawal?

Partial withdrawal of a policy implies withdrawal of only a part of the funds of your policy. For specific details on the same, please refer to the ULIP product brochure in the Products section of this website.

How do I affect a top-up/fund switch/premium redirection?

For Switch and premium redirection, you can download the appropriate form from the Download section of our website, fill it in and send it to the nearest Pramerica Life Insurance branch office. You can log in to the website with your user ID and password and give your request online.

What are top-ups?

Top-ups are one-time payments. You can make an additional investment through a top-up over and above your regular premium payments. You can make a top-up anytime while your policy is in force. The applicable norms for top-ups may differ for every product.

What is premium redirection?

A premium redirection enables you to change your fund allocation for all the future premiums of your policy.

What is a switch?

A switch enables you to shift the existing units of your unit-linked policy into a new fund.

What is a unit?

It is a component of the fund in a ULIP.

What is a unit fund?

The allocated (invested) portions of the premiums, after deducting all the charges and premiums for risk cover under all policies in a particular fund as chosen by the policyholders, are pooled together to form a unit fund.

Can I change the frequency of payment for my policy?

Yes, you can change the premium frequency from low (annual) to a higher frequency (bi-annual or monthly) or vice-versa.

How do I notify a change in address? Or how can I change my policy details?

You have the following options:

- Download the Policy Amendment Form A form from the Download section of our website, fill and send it to us.

- Call our Customer Service Helpline numbers mentioned in the Contact Us section of the website.

- Or write to us at the corporate address mentioned in the Contact Us section of the website

How do I assign a policy or transfer a life insurance policy?

Assignment or transfer of a life insurance policy may be made by simply endorsing that effect in the policy document. Another way of transferring or assigning the life insurance policy is to get a separate assignment deed executed. The former case is the preferred assignment mode as it is exempt from further stamp duty. The assignor should sign an assignment or his duly authorised agent, specifically stating the transfer or assignment. At least one witness should attest the document.

Can I assign a policy?

Yes, you can assign a policy. To assign the policy, you have to notify us regarding the assignment.

What is the transfer or assignment of a life insurance policy?

Transfer or assignment is a method of transferring one's transferable interest in a life insurance policy to another person or institution, for example, as a security for repayment of loans.

What details am I to provide about the nominee(s)?

The following details are necessary when filling in the proposal form:

- Full name of the nominee

- Address

- Age

- The relationship between you and the nominee

Can I change my nomination?

Yes. You can change your nomination at any time till the maturity date. All you need to do is to inform us about the change through the specified form.

What is nomination and who is a nominee?

Nomination is a right conferred on the life insurance policyholder to appoint a person(s) to receive the policy monies if the policy becomes a claim by death. Any policyholder who is a major and the life insured under a policy can make a nomination. A nominee is a person designated by the policyholder to receive the proceeds of an insurance policy, upon the death of the life insured.

What is the difference between nomination and assignment?

While nomination is an authorisation to receive the policy monies in the event of death of the life insured, it does not give the nominee an absolute right over the money received to exclude other legal heirs. Further, the nomination can be revoked or cancelled at any time during the policyholder's lifetime at his will and pleasure or by a subsequent assignment.

On the other hand, the assignment of an insurance policy is a transfer or assignment of all rights and liabilities of the insurance policy in favour of the assignee.

What details am I required to provide about the nominee(s)?

The following details are necessary when filling in the proposal form:

- Full name of the nominee

- Address

- Age

- The relationship between you and the nominee

Disclaimers:

* As on 31st March 2026

** Individual death claims settled and reported in public disclosures for FY 31st March 2026

^ As reported in Annual Report for FY 31st March 2026

# Valid for Pramerica Life Rakshak Smart plan, purchased by serving

Indian Army personnel | Guarantee valid upto Rs 20 Lakhs | Standard

policy T&C apply

*T&C Apply (Illustration for 35 year old healthy male with Premium Payment Term for 12 years and Policy Term 20 years)

.png)

{kind=link}